Conceptual Framework

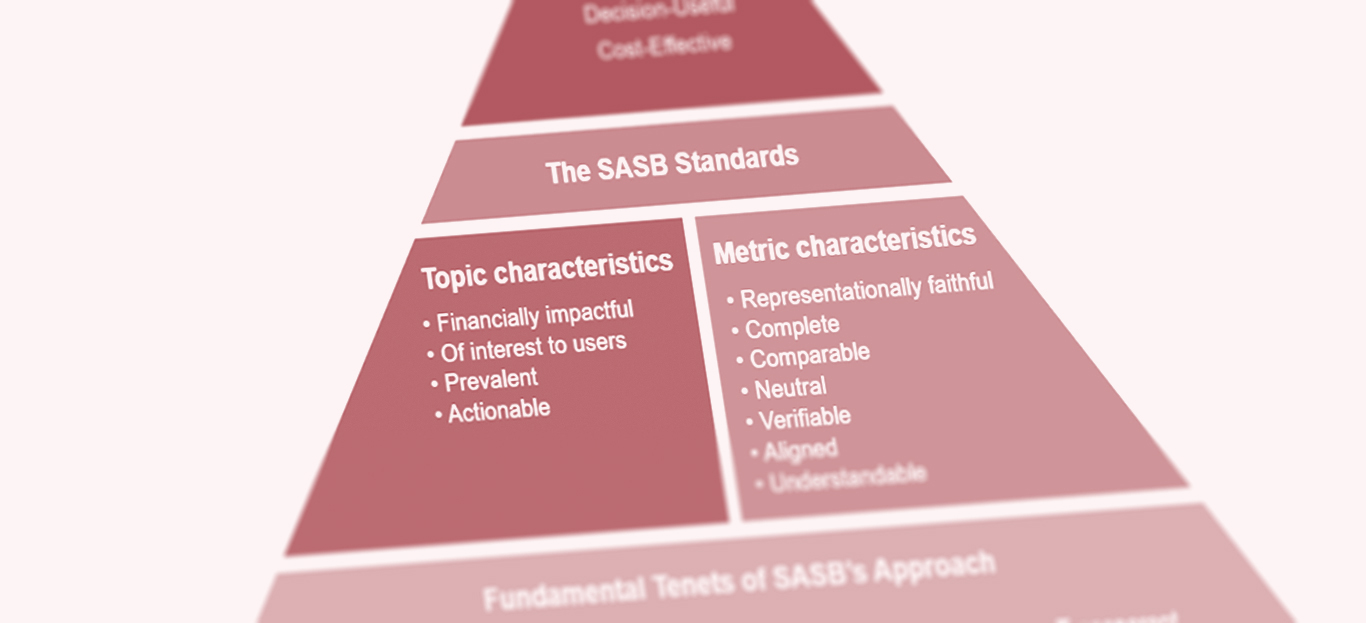

The SASB Conceptual Framework set out the basic concepts, principles, definitions, and objectives that guided the SASB Standards Board in its approach to setting standards for sustainability accounting; it provided an overview of sustainability accounting, describing its objectives and audience.

The SASB Conceptual Framework was in the process of being revised and underwent a public comment period prior to the consolidation of the Value Reporting Foundation into the IFRS Foundation. The Conceptual Framework exposure draft, which was available for public comment from August 28, 2020-December 31, 2020, can be found here. The original, 2017 version of the Conceptual Framework can be found here.

For more information about the process to develop SASB Standards, please read the Rules of Procedure, which established the processes and practices followed by the SASB Standards Board in its standard-setting activities.